The Chinese are intentionally torching their diplomatic relationships with the wider world. The question is why?

The short version is that China’s spasming belligerency is a sign not of confidence and strength, but instead insecurity and weakness. It is an exceedingly appropriate response to the pickle the Chinese find themselves in.

Some of these problems arose because of coronavirus, of course. Chinese trade has collapsed from both the supply and demand sides. In the first quarter of 2020 China experienced its first recession since the reinvention of the Chinese economy under Deng Xiaoping in 1979. Blame for this recession can be fully (and accurately) laid at the feet of China’s coronavirus epidemic. But in Q2 China’s recession is certain to continue because the virus’ spread worldwide means China’s export-led economy doesn’t have anyone to export to.

Nor are China’s recent economic problems limited to coronavirus. One of the first things someone living in a rapidly industrializing economy does once their standard of living increases is purchase a car, but car purchases in China started turning negative nearly two years before coronavirus reared its head.

Why the collapse even in what “should” be happening with the economy? It really comes down to China’s financial model. In the United States (and to a lesser degree, in most of the advanced world) money is an economic good. Something that has value in and of itself, and so it should be applied with a degree of forethought for how efficiently it can be mobilized. This is why banks require collateral and/or business plans before they’ll fund loans.

That’s totally not how it works in China. In China, money – capital, to be more technical – is considered a political good, and it only has value if it can be used to achieve political goals. Common concepts in the advanced world such as rates of return or profit margins simply don’t exist in China, especially for the state owned enterprises (of which there are many) and other favored corporate giants that act as pillars of the economy. Does this generate growth? Sure. Explosive growth? Absolutely. Provide anyone with a bottomless supply of zero (or even subzero) percent loans and of course they’ll be able to employ scads of people and produce tsunamis of products and wash away any and all competition.

This is why China’s economy didn’t slow despite sky-high commodity prices in the 2000s – bottomless lending means Chinese businesses are not price sensitive. This is why Chinese exporters were able to out-compete firms the world over in manufactured goods – bottomless lending enabled them to subsidize their sales. This is why Chinese firms have been able to take over entire industries such as cement and steel fabrication – bottomless lending means the Chinese don’t care about the costs of the inputs or the market conditions for the outputs. This is why the One Belt One Road program has been so far reaching – bottomless lending means the Chinese produce without regard for market, and so don’t get tweaky about dumping product globally, even in locales no one has ever felt the need to build road or rail links to. (I mean, come on, a rail line through a bunch of poor, nearly-marketless post-Soviet ‘Stans’ to dust-poor, absolutely-marketless Afghanistan? Seriously, what does the winner get?)

Investment decisions not driven by the concept of returns tend to add up. Conservatively, corporate debt in China is about 150% of GDP. That doesn’t count federal government debt, or provincial government debt, or local government debt. Nor does it involve the bond market, or non-standard borrowing such as LendingTree-like person-to-person programs, or shadow financing designed to evade even China’s hyper-lax financial regulatory authorities. It doesn’t even include US dollar-denominated debt that cropped up in those rare moments when Beijing took a few baby steps to address the debt issue and so firms sought funds from outside of China. With that sort of attitude towards capital, it shouldn’t come as much of a surprise that China’s stock markets are in essence gambling dens utterly disconnected from issues of supply and labor and markets and logistics and cashflow (and legality). Simply put, in China, debt levels simply are not perceived as an issue.

Until suddenly, catastrophically, they are.

As every country or sector or firm that has followed a similar growth-over-productivity model has discovered, throwing more and more money into the system generates less and less activity. China has undoubtedly past that point where the model generates reasonable outcomes. China’s economy roughly quadrupled in size since 2000, but its debt load has increased by a factor of twenty-four. Since the 2007-2009 financial crisis China has added something like 100% of GDP of new debt, for increasingly middling results.

But more important than high debt levels is that eventually, inevitably, economic reality forces a correction. If this correction happens soon enough, it only takes down a small sliver of the system (think Enron’s death). If the inefficiencies are allowed to fester and expand, they might take down a whole sector (think America’s dot.com bust in 2000). If the distortions get too large, they can spread to other sectors and trigger a broader recession (think America’s 2007 subprime-initiated financial crisis). If they become systemic they can bring down not only the economy, but the political system (think Indonesia’s 1998 government collapse).

It is worse than it sounds. The CCP has long presented the Chinese citizenry with a strict social contract: the CCP enjoys an absolute political monopoly in exchange for providing steadily increasing standards of living. That means no elections. That means no unsanctioned protests. That means never establishing an independent legal or court system which might challenge CCP whim. It means firmly and permanently defining “China’s” interests as those of the CCP.

It makes the system firm, but so very, very brittle. And it means that the CCP fears – reasonably and accurately – that when the piper arrives it will mean the fall of the Party. Knowing full well both that the model is unsustainable and that China’s incarnation of the model is already past the use-by date, the CCP has chosen not to reform the Chinese economy for fear of being consumed by its own population.

The only short-term patch is to quadruple down on the long-term debt-debt-debt strategy that the CCP already knows no longer works, a strategy it has already followed more aggressively and for longer than any country previous, both in absolute and relative terms. The top tier of the Chinese Communist Party (CCP) – and most certainly Xi himself – realize that means China’s inevitable “correction” will be far worse than anything that has happened in any recessionary period anywhere in the world in the past several decades.

And of course that’s not all. China faces plenty of other of issues that range from the strategically hobbling to the truly system-killing.

- China suffers from both poor soils and a drought-and-floodprone climatic geography. Its farmers can only keep China fed by applying five times the inputs of the global norm. This only works with, you guessed it, bottomless financing. So when China’s financial model inevitably fails, the country won’t simply suffer a subprime-style collapse in ever subsector simultaneously, it will face famine.

- The archipelagic nature of the East Asian geography fences China off from the wider world, making economic access to it impossible without the very specific American-maintained global security environment of the past few decades.

- China’s navy is largely designed around capturing a very specific bit of this First Island Chain, the island of Formosa (aka the country of Taiwan, aka the “rebellious Chinese province”). Problem is, China’s cruise-missile-heavy, short-range navy is utterly incapable of protecting China’s global supply chains, making China’s export-led economic model questionable at best.

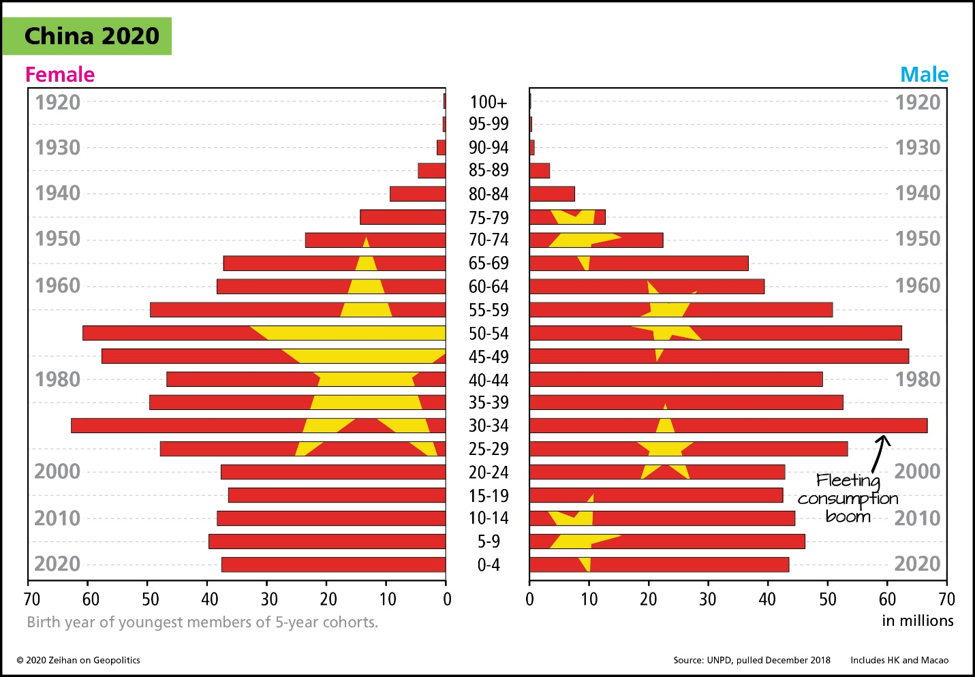

- Nor is home consumption an option. Pushing four decades of the One Child Policy means China has not only gutted its population growth and made the transition to a consumption-led economy technically impossible, but has now gone so far to bring the entire concept of “China” into question in the long-term.

|

|